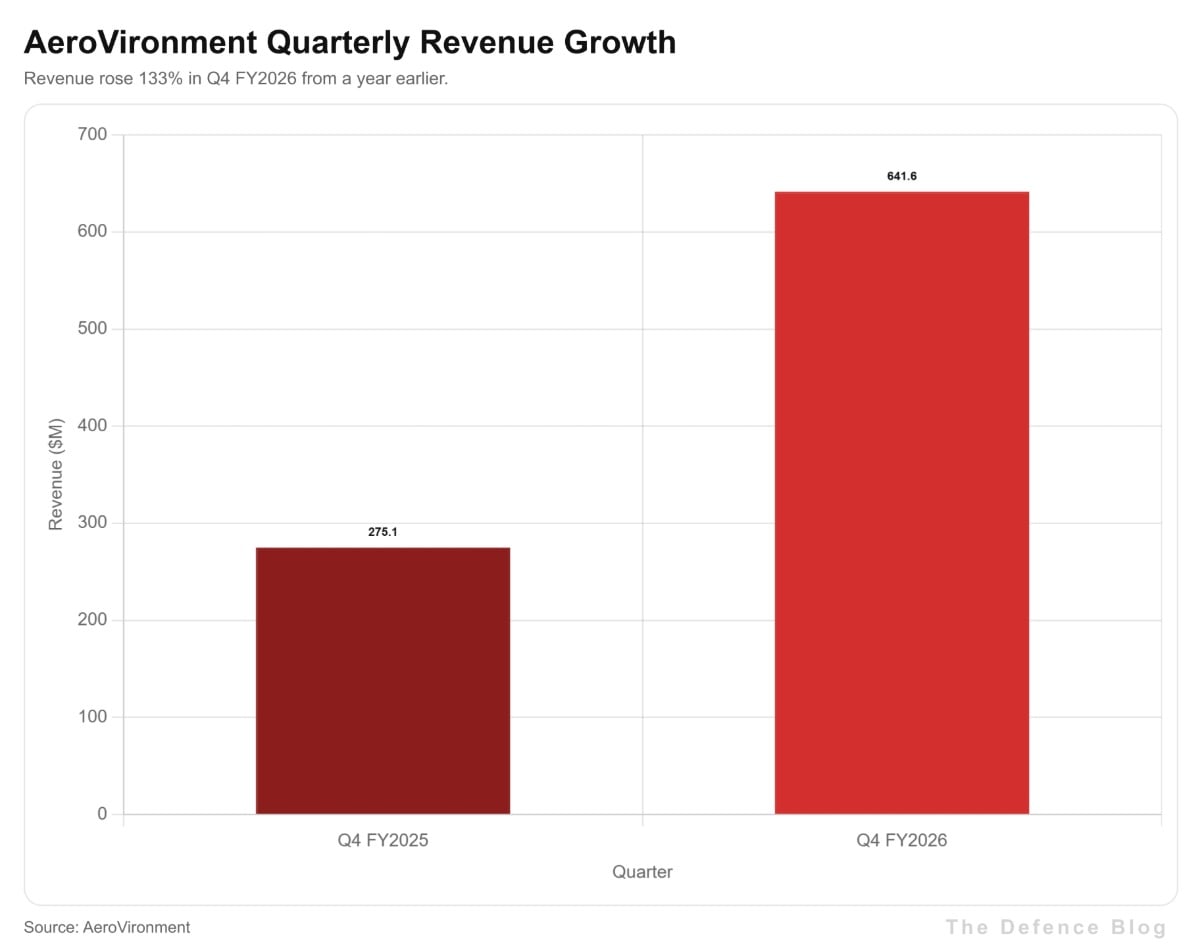

- AeroVironment reported fiscal fourth quarter revenue of $641.6 million, up 133 percent, and full year revenue near $2 billion.

- Funded backlog reached $1.2 billion as of April 30, 2026, while the company posted a full year GAAP net loss of $265.1 million.

AeroVironment (AV) posted fourth-quarter revenue growth of 133 percent, pulling in $641.6 million and pushing full fiscal year revenue to nearly $2 billion, a jump the drone maker says was driven by soaring demand for attack drones, counter-drone defenses, and the space and cyber technology it picked up in its biggest acquisition ever.

The company reported the results for the quarter and fiscal year ended April 30, 2026, in a filing released June 29, and the numbers mark the clearest evidence yet that a company once known mainly for small loitering munitions has reshaped itself into a much broader defense technology supplier in the span of about 14 months.

AeroVironment built its reputation on the Switchblade family of loitering munitions, compact attack drones that a soldier can carry in a backpack and launch by hand, fly toward a target using an onboard camera, and detonate on impact, a category of weapon that Ukrainian forces have used extensively against Russian armor and that has become one of the defining images of drone warfare over the past several years. That business alone would explain healthy growth, but the bigger driver behind this quarter’s numbers was the company’s acquisition of BlueHalo, a $4.1 billion deal that closed on May 1, 2025, and added space systems, cyber warfare tools, and directed energy weapons to AeroVironment’s lineup almost overnight.

Combined with a smaller acquisition of Empirical Systems Aerospace that closed on March 16, 2026, those two deals contributed $282.3 million of the $641.6 million AeroVironment reported for the quarter, meaning roughly 44 percent of the quarter’s revenue came from businesses AeroVironment did not even own a year earlier.

“Fiscal 2026 marked a transformational year for AV, which included the completion of our largest acquisition, meaningful investments toward diversifying our portfolio in critical areas aligned to our customer’s highest priorities, and the strongest financial performance in our history,” said Wahid Nawabi, AeroVironment’s chairman, president and chief executive officer.

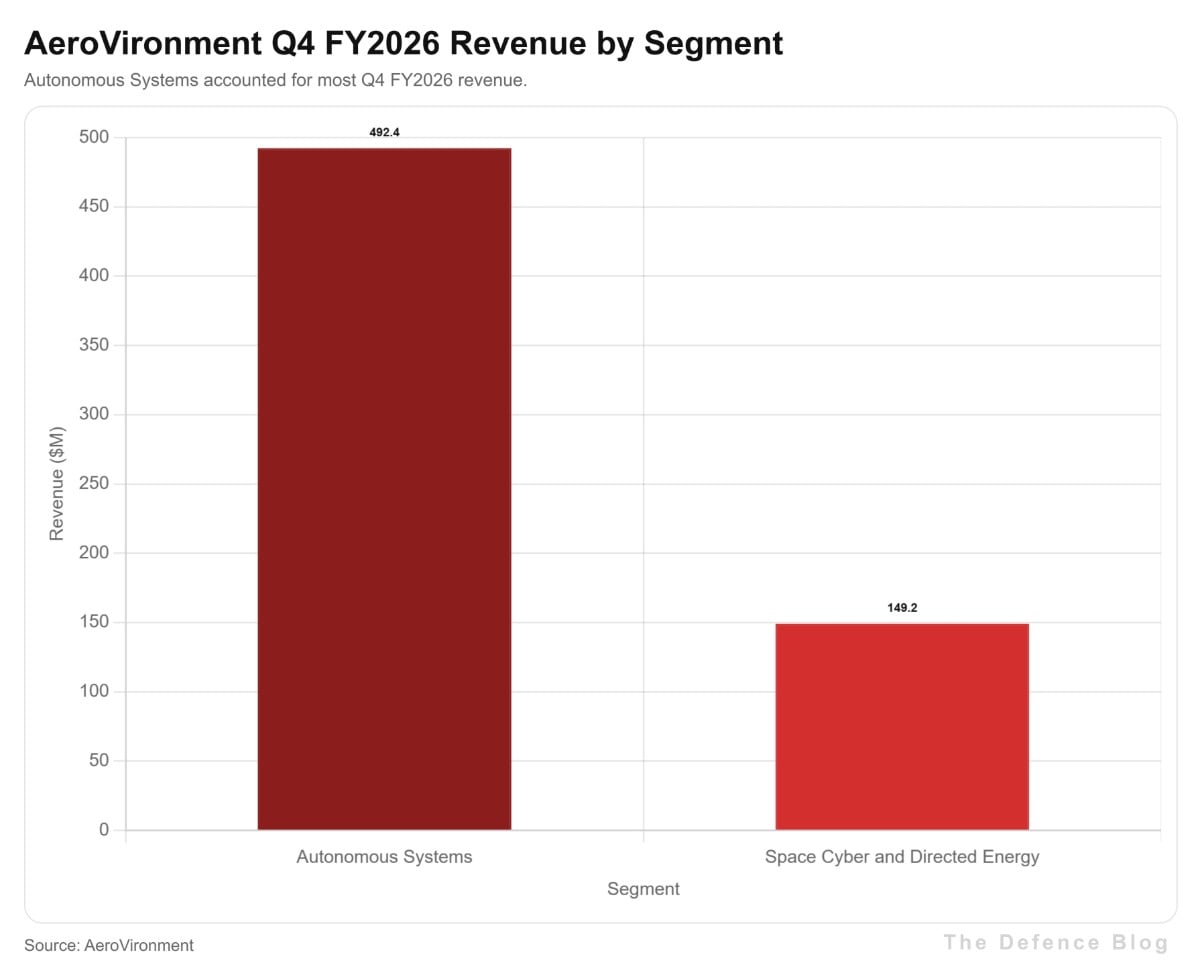

Nawabi’s reference to a diversified portfolio points to how AeroVironment now organizes its business. The company splits its results into two segments, Autonomous Systems, which covers drones and loitering munitions like Switchblade and brought in $492.4 million for the quarter, and Space, Cyber and Directed Energy, the unit built largely around the BlueHalo acquisition, which added $149.2 million. That second segment includes AeroVironment’s Titan family of radio frequency jamming systems for knocking drones out of the sky without firing a shot, a counter-drone business that generated roughly $200 million across the full fiscal year, a modest slice of the company’s overall revenue for now but one Nawabi has told investors could grow two to three times larger within the next three to five years as militaries worldwide race to field defenses against the same kind of cheap, mass-produced drones that made Switchblade a household name in defense circles.

“We are confident our proven ability to deliver at speed will continue to drive opportunities for AV across our global customer base. We remain focused on executing with excellence and strengthening our supply chain to accelerate the commercialization of our platforms. AV is well-positioned to capture the rising global demand across lethal and non-lethal drones, counter-UAS, space and advanced technologies and deliver long-term shareholder value,” Nawabi said.

The headline revenue growth comes with a less flattering number buried in the filing that any informed investor would want to see alongside it. AeroVironment reported a fourth quarter net income of $63.2 million, a solid rebound from $16.7 million a year earlier, but the company’s full fiscal year still closed with a GAAP net loss of $265.1 million, driven primarily by a $240.7 million goodwill impairment tied to the BlueHalo integration along with heavy non-cash amortization of the intangible assets acquired in that deal. Goodwill impairment is an accounting adjustment companies take when an acquired business turns out to be worth less on paper than what was originally paid for it, and while it does not represent cash leaving the company, a charge of that size signals that integrating a $4.1 billion acquisition into an existing drone business came with real costs and complications along the way, even as the underlying revenue growth remained strong.

Beyond the current quarter, the strongest signal of where AeroVironment’s business is headed sits in its backlog, the total value of contracts the company has already signed but not yet delivered or fully funded. Funded backlog, meaning the portion of that backlog where a customer has actually appropriated money to pay for it, stood at $1.2 billion as of April 30, 2026, up sharply from $726.6 million a year earlier, while total bookings for the fiscal year reached $2.7 billion against a book-to-bill ratio of 1.4, meaning the company won new orders worth 40 percent more than the revenue it recognized over the same period. A book-to-bill ratio above 1.0 generally signals a growing order pipeline rather than a company coasting on work it already completed, and AeroVironment’s ratio suggests demand for its drones, jammers, and space and cyber systems is still outpacing what the company has managed to deliver so far.

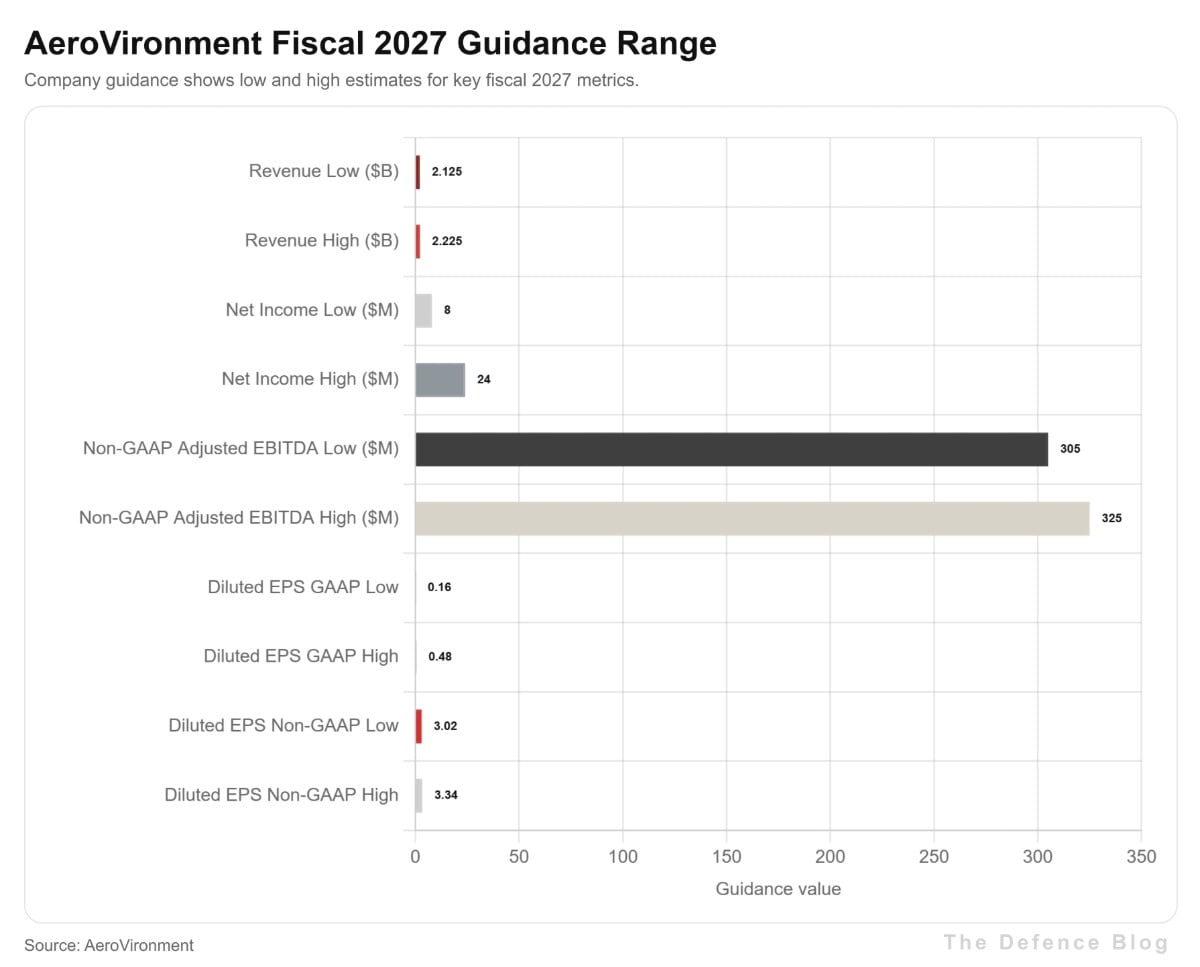

Looking ahead, AeroVironment told investors it expects fiscal 2027 revenue of between $2.125 billion and $2.225 billion, alongside net income of between $8 million and $24 million and non-GAAP adjusted earnings per share of between $3.02 and $3.34. That guidance points to a company expecting continued double-digit revenue growth while working through the accounting drag from its BlueHalo integration, and management was explicit that the estimates depend on factors ranging from government spending decisions to how efficiently the company folds its newly acquired businesses into its existing operations.

AeroVironment’s chief executive has framed the moment in broader terms than a single earnings report, telling investors that conflicts in Ukraine and Iran have permanently changed how militaries think about warfare, with cheap, attritable drones on one side of the fight and increasingly urgent demand for ways to knock them out of the sky on the other. Whether AeroVironment can convert that shift into sustained profit, rather than a revenue chart inflated by acquisition accounting, will depend on how cleanly the company digests BlueHalo over the next few fiscal years, and Wall Street will be watching the goodwill line just as closely as the top line to find out.